10.06.2014, 10am

The VIX index is near its historically lowest levels, while the CVIX (the VIX index for currencies) fell to an all-time low of 5.51. Low volatility favors the strategy of borrowing in currencies with low interest rates and investing the proceeds in higher-yielding currencies, known as carry trades. In my view, it seems that the common currency has started becoming a funding currency for use in such trades. That would imply a sustained depreciation is likely.

Meanwhile, Eurozone’s Sentix investor confidence index fell to 8.5 in June from 12.8 in May, confounding expectations for a jump to 13.2, while the greenback continued to see support on solid US employment data. The ECB’s recent decision to loosen policy alongside expectations for the Federal Reserve to continue scaling back its monthly purchases this year was reflected in the markets on Monday, weakening the euro and strengthening the dollar.

The Canadian dollar was the main winner after Canada’s housing starts for May came at 198k, exceeding market estimates of 185k. This suggest that housing will contribute to the nation’s economic growth in the second quarter after a harsh winter halted construction.

WTI climbed near the 105.00 zone ahead of the API and EIA reports. While no forecast is available for the American Petroleum Institute report that is published today, on Wednesday, the EIA is expected to report that crude stockpiles have declined for a second week in the US. Moreover, Chinese exports have grown and US employment is back at its pre-recession peak, and this is likely to lead to higher oil demand from the world’s two biggest oil consumers.

Overnight, the Aussie strengthened after both the Chinese CPI and PPI rates accelerated in May, reducing the signs that China is sliding into the deflation. This should reduce expectations for the PBOC to roll out more aggressive monetary easing.

As for today, we get industrial production data from France, Italy and the UK, all for April. All three IPs are estimated to have risen on a mom basis, after declining the previous month. The UK industrial output is expected to be the most important one. Continued strength in manufacturing production could have contributed to a healthy pick-up in the overall industrial output. Manufacturing production has risen for four consecutive quarters, and expectations point to further growth ahead. From Italy, we also get the final GDP for Q1. The final forecast is the same as the initial estimate. Switzerland’s unemployment rate is estimated to have declined to 3.1% from 3.2%, while in Norway, both the headline and the underlying CPI rates are forecast to have declined in May.

In the US, the JOLTS (job openings and labor turnover survey) jobs openings are forecast to have risen in April, while wholesale inventories for the same month are expected to have slowed. However, neither release is a major market affecting event.

We have four speakers scheduled on Tuesday. ECB Executive Board member Yves Mersch speaks at a panel discussion, ECB Governing Council member Erkii Liikanen speaks at a Bank of Finland quarterly press briefing, while ECB Governing Council member and head of Slovak Central Bank Jozef Makuch holds a press conference on economic forecasts. RBA Governor Glenn Stevens speaks at the Federal Reserve Bank of San Francisco’s symposium.

The Market

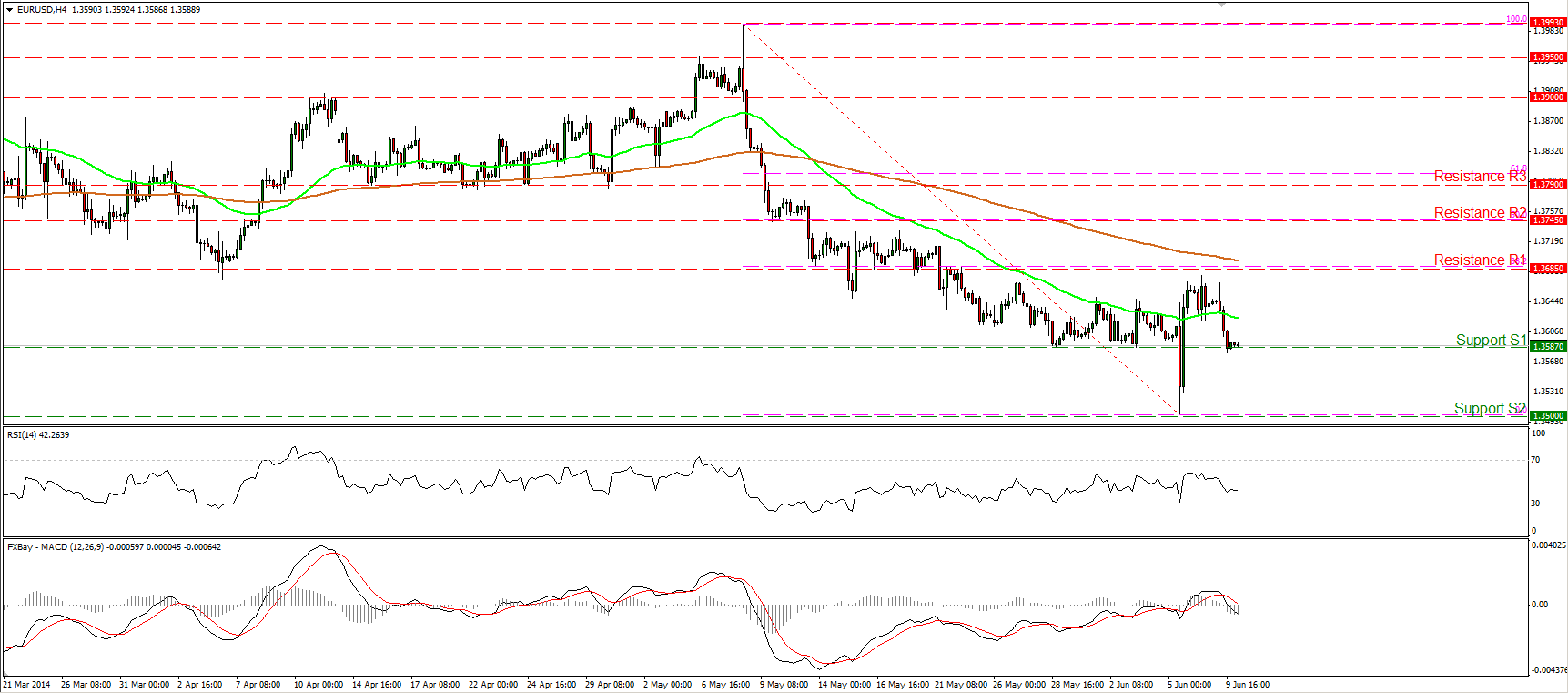

EUR/USD falls to find support at 1.3587

EUR/USD fell sharply on Monday after finding resistance slightly below 1.3685 (R1), the 38.2% retracement level of the 8th May-5th June decline. However, the decline was halted by the support barrier of 1.3587 (S1). A clear dip below that hurdle may signal that Thursday’s advance was just a 38.2% retracement of the aforementioned decline and could target again the key support of 1.3500 (S2). The MACD fell below both its signal and zero lines, confirming yesterday’s bearish momentum.

• Support: 1.3587(S1), 1.3500 (S2), 1.3475 (S3).

• Resistance: 1.3685 (R1), 1.3745 (R2), 1.3790 (R3).

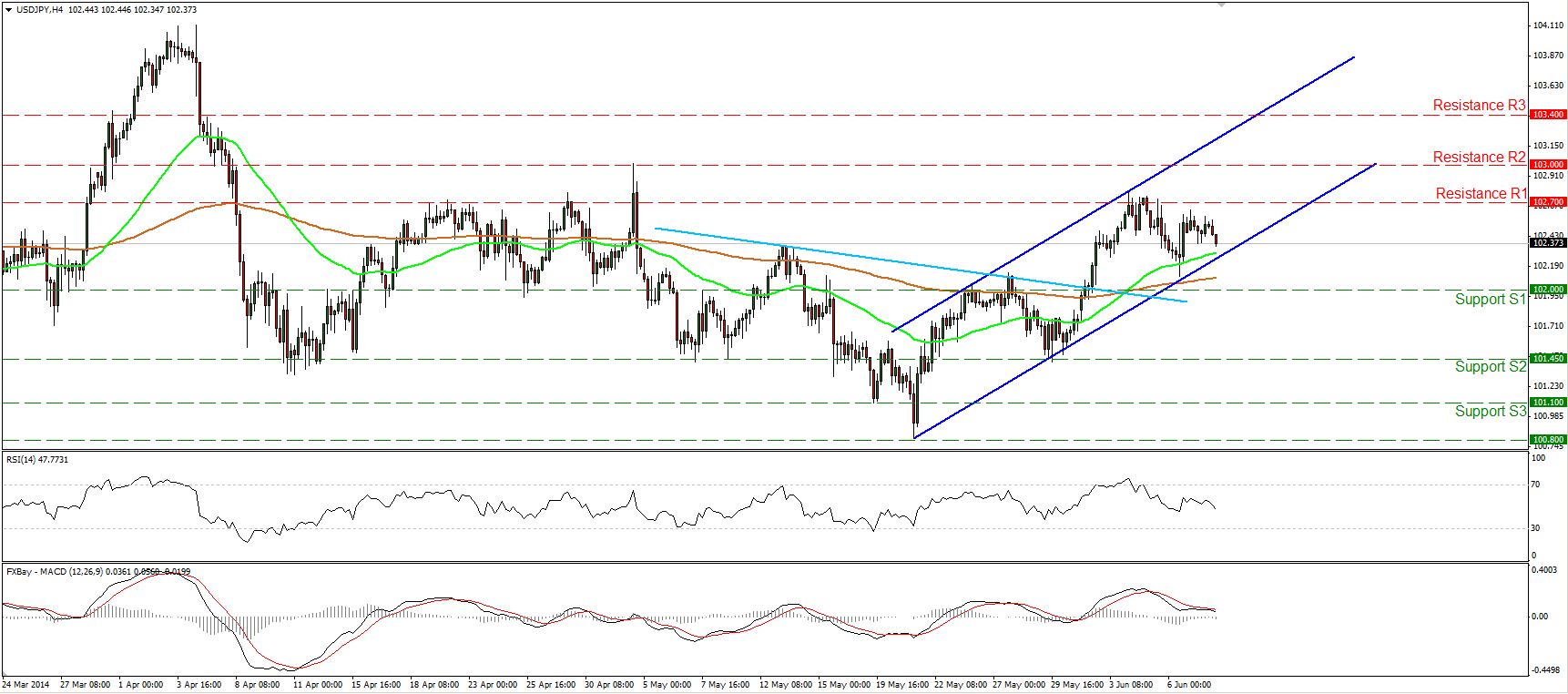

USD/JPY turns neutral

USD/JPY failed to continue its Friday’s advance and moved lower forming a lower high. However, the rate remains within the blue uptrend channel and above both the moving averages, thus I would change my view from positive to neutral for now. A clear move below the 102.00 (S1) zone would signal the completion of a failure swing top formation and turn the picture negative. On the other hand, we need a decisive violation of the 102.70 (R1) resistance zone to have the reinforcement of the uptrend.

• Support: 102.00 (S1), 101.45 (S2), 101.10 (S3).

• Resistance: 102.70 (R1), 103.00 (R2), 103.40 (R3).

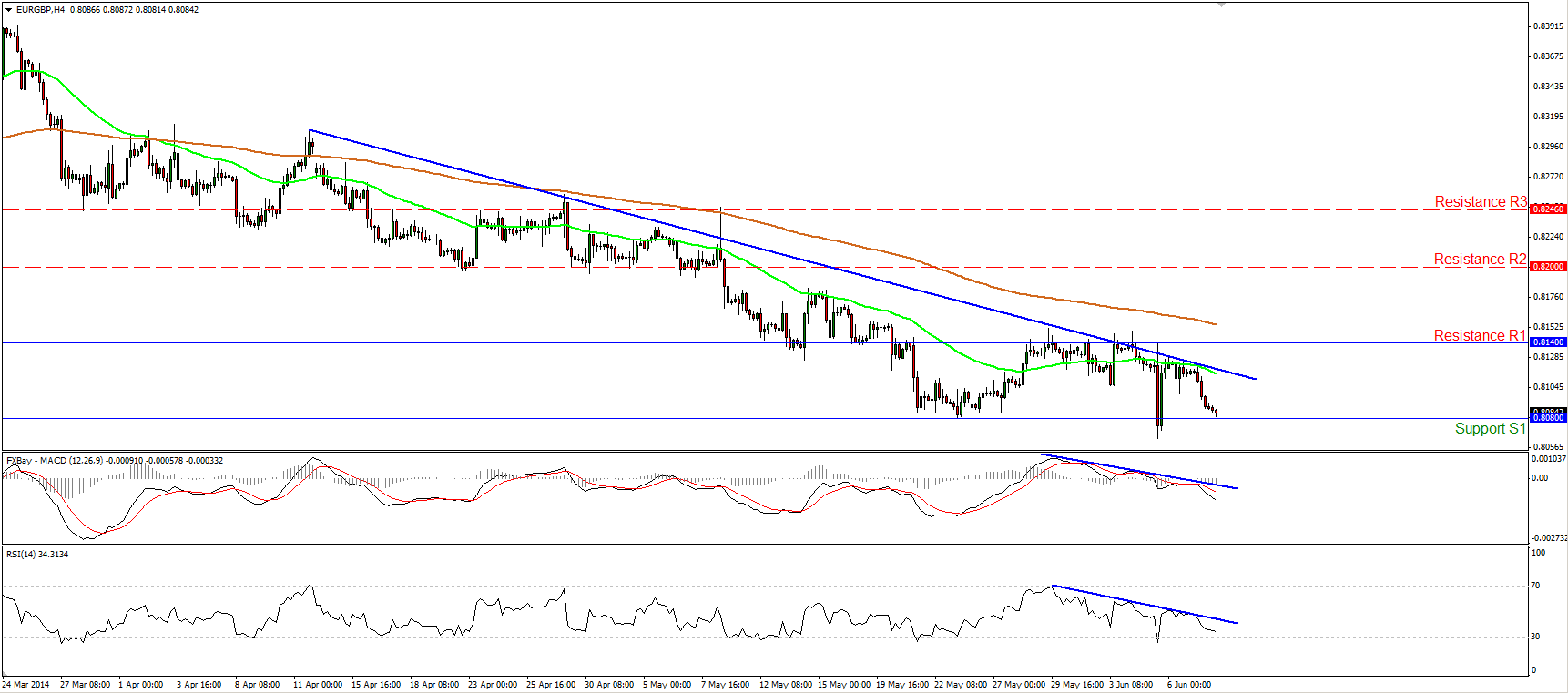

EUR/GBP finds support at 0.8080

EUR/GBP met resistance at the blue downtrend line and declined to find support at the 0.8080 (S1) zone. Although both our momentum studies continue their downward paths, remaining below their blue resistance lines, I would maintain my neutral view for now as the rate oscillates between the support of 0.8080 (S1) and the resistance of 0.8140 (R1) since the 20th of May. Only a decisive dip below the 0.8080 (S1) barrier would confirm a forthcoming lower low and signal the reinforcement of the downtrend.

• Support: 0.8080 (S1), 0.8035 (S2), 0.8000 (S3).

• Resistance: 0.8140 (R1), 0.8200 (R2), 0.8246 (R3).

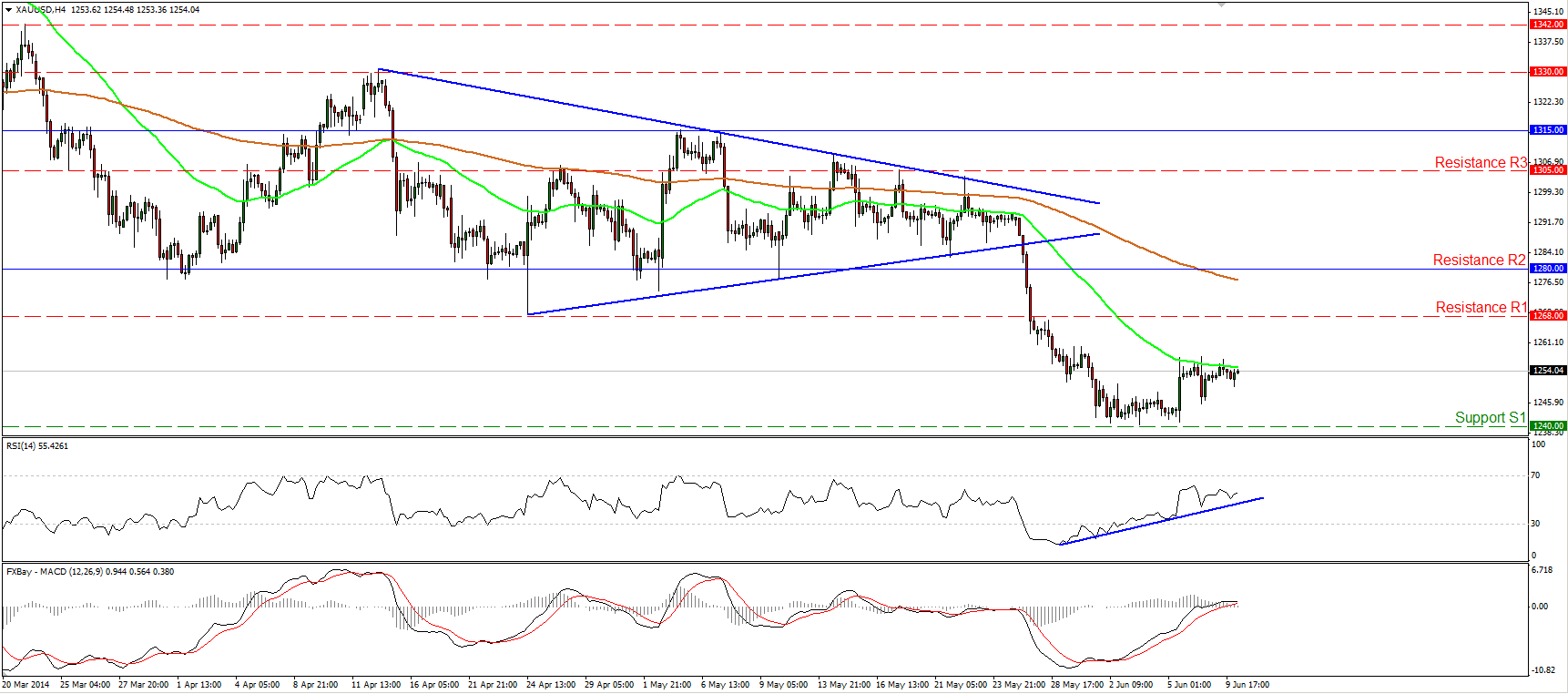

Gold remains near the 50-period MA

Gold continued consolidating on Monday, remaining below the 50-period moving average. Considering that the MACD lies above both its signal and zero lines and that the RSI continues its upside path, I cannot rule out further advance, maybe for a test near the 1268 (R1) zone. Nonetheless, since the possibility for a lower high still exists, I would consider the recent upside wave as a retracement before the bears prevail again.

• Support: 1240 (S1), 1218 (S2), 1200 (S3) .

• Resistance: 1268 (R1), 1280 (R2), 1305 (R3).

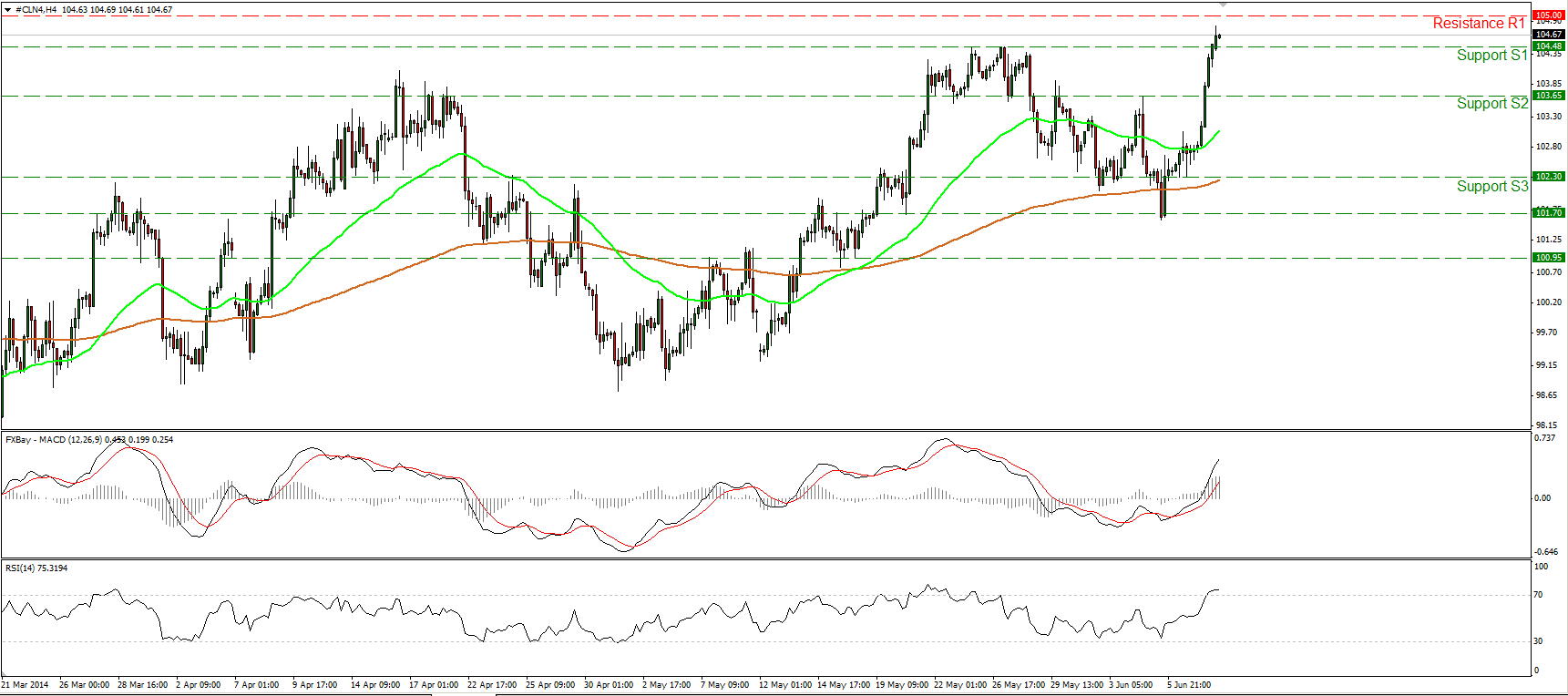

WTI climbs near the 105.00 zone

WTI surged on Monday, violating two resistance hurdles in a row. The price managed to overcome the highs of May at 104.48 and is now heading towards the psychological zone of 105.00 (R1). The MACD lies above both its signal and zero lines, confirming yesterday’s strong positive momentum, but the RSI lies within its overbought territory, showing signs of topping. As a result, I cannot rule out some consolidation or a forthcoming pullback in the near future. However, the overall short-term picture is to the upside and a clear move above 105.00 (R1) could pave the way towards the zone of 108.00 (R2).

• Support: 104.48 (S1), 103.65 (S2), 102.35 (S3).

• Resistance: 105.00 (R1), 108.00 (R2), 110.00 (R3).

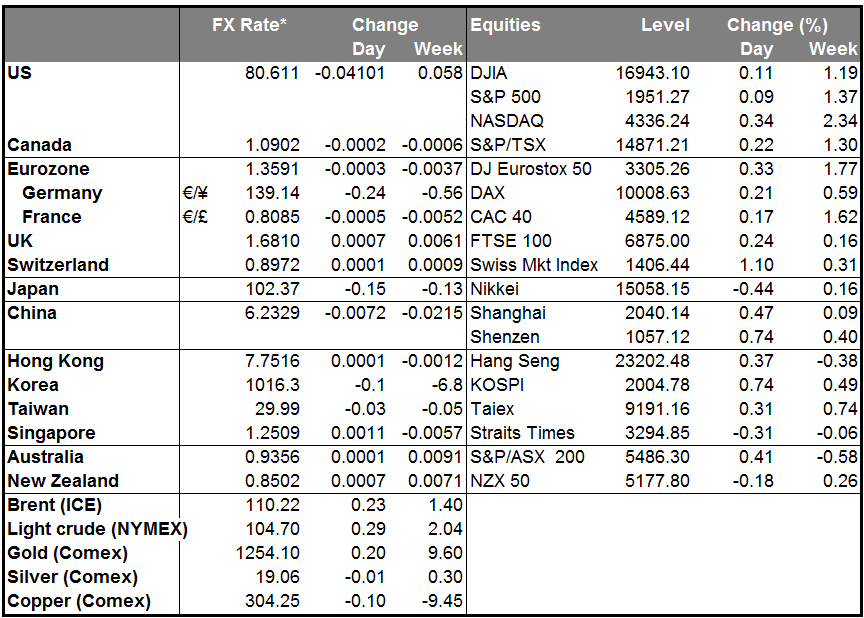

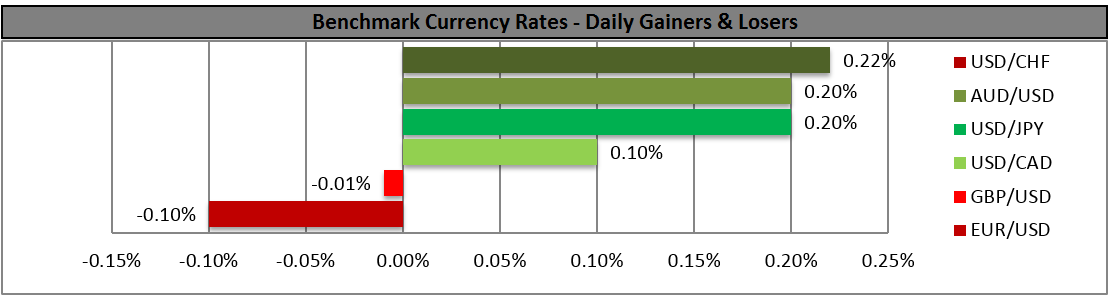

BENCHMARK CURRENCY RATES – DAILY GAINERS AND LOSERS

MARKETS SUMMARY